5 Common Credit Card Myths Debunked in 2026: Financial Misconceptions That Cost You Money

November 21, 2025

5 Common Credit Card Myths Debunked in 2026: Financial Misconceptions That Cost You Money

Credit cards are powerful financial tools, but their complexity has given rise to a persistent host of misconceptions. These myths, often passed down through generations or spread on outdated forums, can lead US consumers to make costly financial mistakes, damaging their credit scores and increasing their interest expenses. In 2026, navigating the credit landscape requires clear, factual information. This comprehensive guide will tackle 5 common credit card myths debunked, separating financial fact from fiction and equipping you with the truth needed to use your credit cards strategically for financial success.

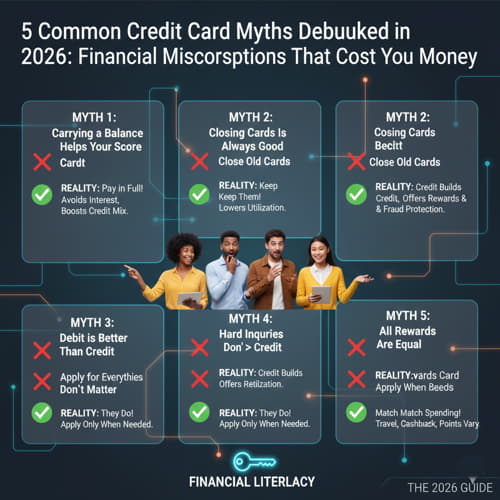

Myth 1: Carrying a Balance Helps Your Credit Score

Myth 1: Carrying a Balance Helps Your Credit Score

This is perhaps the most persistent and financially destructive credit card myth.

First Time Offense Credit Card Theft 2026: Laws & Consequences

Credit Cards and Technology: Your 2026 Guide to Digital Payments