What Happens If I Only Pay the Minimum on My Credit Card in 2026? The Costly Truth

What Happens If I Only Pay the Minimum on My Credit Card in 2026? The Costly Truth

For many US consumers facing high credit card balances, making only the minimum payment due can feel like a lifeline—a way to manage immediate expenses without defaulting. However, this seemingly innocuous act is, in reality, a deceptive financial trap. Understanding what happens if I only pay the minimum on my credit card is paramount, as this habit is one of the quickest ways to accumulate crippling debt, destroy your credit score, and dramatically extend your repayment timeline. In 2026, with average credit card APRs hovering around 20% or more, consistently paying only the minimum can translate into thousands of dollars in avoidable interest and years of financial struggle. This comprehensive guide will expose the costly truth behind minimum payments, detailing their devastating impact on your finances and providing a clear path to break free from this insidious cycle.

1. The Minimum Payment: A Deceptive Lifeline

1. The Minimum Payment: A Deceptive Lifeline

Credit card issuers design minimum payments to be low enough to seem manageable, but high enough to ensure they collect substantial interest over a long period.

The Composition of a Minimum Payment:

A typical minimum payment is often:

-

1-3% of your outstanding balance (often with a floor, e.g., $25).

-

Plus any accrued interest from the previous billing cycle.

-

Plus any fees (e.g., late fees from prior months).

The Problem: The bulk of your minimum payment often goes to interest and fees, leaving very little to reduce your principal balance.

2. The Compounding Interest Nightmare

This is the most significant and immediate consequence of only paying the minimum.

A. Endless Interest Accumulation

-

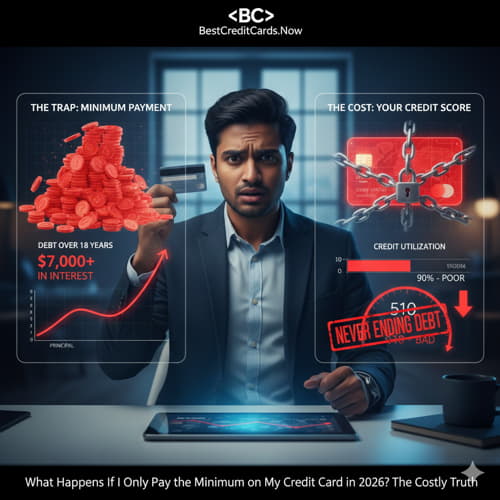

Scenario: You have a $5,000 balance with a 22% APR and a 2% minimum payment.

-

First Month: Your minimum payment is $100. Of that, roughly $91 goes to interest, and only $9 goes to principal.

-

The Cost: Because you haven’t paid off the full balance, you forfeit the Understanding Credit Card Grace Period Meaning. Interest immediately begins accruing on new purchases from the transaction date. This means you’re paying interest on your old debt AND new purchases, creating a vicious cycle.

-

The Math: A $5,000 balance at 22% APR, making only 2% minimum payments, could take over 18 years to pay off and cost more than $7,000 in interest—more than the original debt!

B. The Illusion of Affordability

The low minimum payment makes it feel like you can afford the debt, preventing you from addressing the underlying issue of overspending or lack of budgeting. This false sense of security leads to further reliance on credit.

3. Devastating Impact on Your Credit Score

Beyond the interest cost, only paying the minimum can severely damage your credit profile.

A. High Credit Utilization Ratio (CUR)

-

The Problem: Your Credit Utilization Ratio (CUR)—the amount of credit you use versus your total available credit—accounts for 30% of your FICO score. Consistently paying only the minimum means your balances remain high, keeping your CUR elevated (e.g., above 30%, or even 50%+).

-

The Consequence: A high CUR is a major red flag for lenders and will significantly lower your credit score, making it harder to qualify for new loans (like mortgages or auto loans) or new credit cards with favorable terms.

-

The Cycle: A lower credit score means you qualify for worse interest rates on future loans, perpetuating financial struggle. To understand how utilization impacts your score, you should learn How to Improve My Credit Score from 500 to 700.

B. Longer Debt Recovery Timeline

As illustrated in the example above, a small debt can take nearly two decades to pay off. This prolonged debt means a longer period where your financial flexibility is limited, and you remain beholden to creditors.

4. The Road to Recovery: Breaking the Minimum Payment Cycle

If you’re caught in the minimum payment trap, here’s how to break free:

1. Stop Accumulating New Debt: This is non-negotiable. Put the credit cards away. 2. Pay More Than the Minimum: Even an extra $10 or $20 above the minimum can significantly reduce the repayment timeline and total interest paid. 3. Create a Budget: Track your income and expenses to identify where you can cut back to free up more money for debt payments. 4. Debt Snowball or Avalanche: Choose a debt repayment strategy. * Snowball: Pay off your smallest debt first for psychological wins. * Avalanche: Pay off the debt with the highest interest rate first to save the most money. For a detailed strategy on this, consult our guide, Best Way to Pay Off High Interest Credit Card Debt. 5. Consider Debt Consolidation: If you have multiple high-interest debts, consider a balance transfer credit card (with a 0% intro APR) or a personal loan to lower your interest rate and simplify payments. This is an excellent option for managing multiple debts.

In conclusion, what happens if I only pay the minimum on my credit card is a slow, costly process that benefits the bank, not you. It leads to escalating interest, extended debt, and a damaged credit score. By making a conscious effort to pay more than the minimum and adopting a proactive debt repayment strategy, you can escape this trap and regain control of your financial future in 2026.

Credit Cards for Specific Life Stages: Your 2026 Tailored Guide

Credit Card Points vs. Cash Back: The Definitive 2026 Value-Driven