Personal Loan vs Credit Card for Major Purchases in 2026: Choosing the Right Debt for Your Needs

Personal Loan vs Credit Card for Major Purchases in 2026: Choosing the Right Debt for Your Needs

In 2026, many US consumers face the challenge of financing major purchases, whether it’s a home renovation, medical expenses, a significant appliance upgrade, or debt consolidation. The two most common and accessible options are a personal loan or a credit card. Deciding between a personal loan vs credit card for major purchases is a critical financial choice that can significantly impact your interest costs, repayment timeline, and overall financial health. There’s no universal “better” option; the ideal choice depends on the size of the purchase, your credit score, current interest rates, and your repayment discipline. This comprehensive guide will dissect the pros and cons of each financing method, providing a clear framework to help you make the smartest decision for your specific financial situation.

1. Understanding Personal Loans: Structured and Predictable

1. Understanding Personal Loans: Structured and Predictable

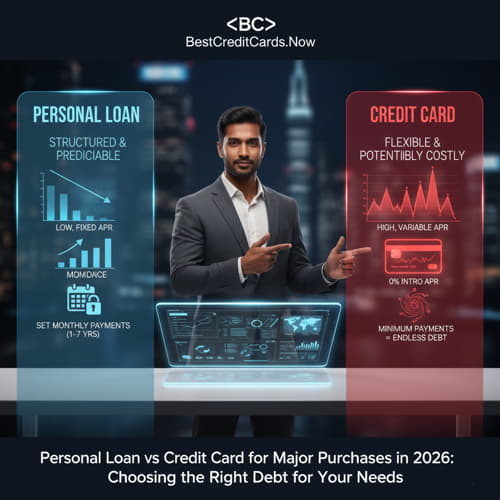

A personal loan is an unsecured loan (meaning it doesn’t require collateral like a house or car) issued by a bank, credit union, or online lender.

A. Key Characteristics:

-

Fixed Interest Rate: The interest rate remains the same for the entire loan term, providing predictability.

-

Fixed Monthly Payments: You pay the same amount each month until the loan is fully repaid.

-

Set Repayment Term: Loans typically range from 1 to 7 years.

-

Lump Sum Disbursement: You receive the entire loan amount upfront, which you then use for your purchase.

B. Pros of Personal Loans for Major Purchases:

-

Lower Interest Rates: Often significantly lower than credit card APRs, especially for consumers with good credit (e.g., 6% to 15% vs. 18% to 28% for credit cards).

-

Predictable Repayment: Fixed payments and terms make budgeting easier. You know exactly when the debt will be paid off.

-

No Temptation to Overspend: You get a set amount of money; there’s no revolving credit line to tap into repeatedly.

-

Potential for Debt Consolidation: Personal loans are excellent for combining multiple high-interest credit card debts into one lower-interest, fixed payment.

C. Cons of Personal Loans:

-

Origination Fees: Some lenders charge an upfront fee (1% to 8% of the loan amount) to process the loan, which can reduce the amount you actually receive.

-

Hard Credit Inquiry: Applying results in a hard inquiry on your credit report, which can slightly lower your score temporarily.

-

Rigid Payment Schedule: Missing payments can lead to late fees and damage your credit score, just like credit cards.

2. Understanding Credit Cards: Flexible but Potentially Costly

A credit card provides a revolving line of credit that you can use, pay off, and reuse.

A. Key Characteristics:

-

Revolving Credit: You can spend up to your credit limit, pay it off, and then spend again.

-

Variable Interest Rate: APRs can fluctuate, though many are fixed for specific periods.

-

Minimum Payments: You are required to pay only a small percentage of your balance each month.

-

No Fixed Term: If you only make minimum payments, it can take decades to pay off debt, as detailed in What Happens If I Only Pay the Minimum on My Credit Card.

B. Pros of Credit Cards for Major Purchases:

-

0% Introductory APR Offers: Many cards offer 0% interest for 12 to 21 months on new purchases. This is the most compelling reason to use a credit card for a major purchase if you can pay it off within that promotional period.

-

Rewards and Cash Back: You can earn points, miles, or cash back on your purchase, effectively reducing its cost.

-

Flexibility: You can pay off the debt faster than a personal loan’s fixed schedule if you choose.

-

Fraud Protection: Credit cards typically offer stronger fraud protection than debit cards, which is why understanding Zero Liability Policy Credit Card Meaning is so important.

C. Cons of Credit Cards:

-

High Standard APRs: Once the 0% intro APR expires (or if you don’t qualify for one), credit card interest rates are often much higher than personal loan rates.

-

Temptation to Overspend: The revolving nature of credit can make it easy to accumulate more debt.

-

Damage to Credit Utilization: A large purchase can significantly increase your credit utilization ratio, which can harm your credit score.

3. When to Choose Which Option (2026 Strategy)

The choice hinges on your repayment capability and the nature of the purchase.

What Happens If I Only Pay the Minimum on My Credit Card? The Trap of Long-Term Debt

Credit Card Balance Transfer vs Personal Loan: The 2026 Guide to Debt Consolidation