How to Dispute a Credit Card Charge in 2026

How to Dispute a Credit Card Charge in 2026: Your Essential Consumer Protection Guide

In 2026, credit cards remain a cornerstone of American commerce, offering convenience, rewards, and robust security. However, despite their advantages, consumers occasionally encounter erroneous or fraudulent transactions. Whether it’s an unrecognized charge, a double billing, a service not rendered, or a product never received, knowing how to dispute a credit card charge is a fundamental skill for every cardholder. This process, governed by federal laws like the Fair Credit Billing Act (FCBA), is your primary defense against financial loss and merchant disputes. This comprehensive guide will walk you through the precise steps to successfully dispute a credit card charge, clarify your consumer rights, and provide the critical strategies to ensure your financial integrity in an increasingly digital world.

1. Understanding Your Rights: The Fair Credit Billing Act (FCBA)

1. Understanding Your Rights: The Fair Credit Billing Act (FCBA)

The FCBA is a federal law that provides protections for consumers against billing errors and outlines a clear process for resolving disputes. It applies to “open-end” credit accounts, which includes most credit cards.

What Constitutes a “Billing Error” under FCBA?

-

Unauthorized Charges: Charges you did not make or authorize. This is where your Zero Liability Policy Credit Card Meaning comes into play.

-

Incorrect Charges: A charge for the wrong amount or on the wrong date.

-

Undelivered Goods/Services: Goods or services that were not delivered as agreed upon.

-

Goods/Services Not Accepted: Defective goods, or services that were not provided to your satisfaction (provided you made a good faith effort to resolve with the merchant).

-

Mathematical Errors: Miscalculations in your bill.

-

Failure to Post Payments: Payments you made but were not credited to your account.

-

Charges for which you requested documentation: If you ask for proof of a charge and don’t receive it.

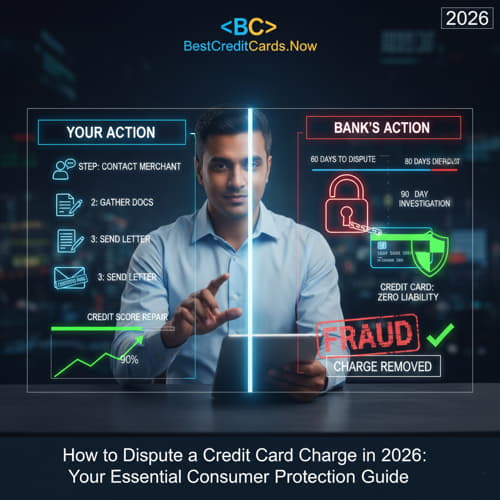

2. The Critical Timeline: Act Quickly!

The FCBA specifies strict deadlines for disputing a charge. Miss these, and you could lose your protections.

-

60 Days: You must send your written dispute notice within 60 days after the first bill containing the error was mailed to you.

-

90 Days (Investigation): The card issuer must acknowledge your dispute within 30 days and resolve it within two billing cycles (but no more than 90 days).

3. Step-by-Step Guide: How to Dispute a Credit Card Charge

Follow these steps meticulously to maximize your chances of a successful dispute.

Step 1: Contact the Merchant First (Optional but Recommended)

Before formally disputing with your card issuer, try to resolve the issue directly with the merchant. This can often be the quickest solution for simple errors or misunderstandings. Keep a record of all communications (dates, times, names of representatives, what was discussed).

Step 2: Gather All Documentation

Collect any evidence related to the disputed charge:

-

Receipts or order confirmations.

-

Correspondence with the merchant (emails, chat logs, call notes).

-

Screenshots of product descriptions or terms.

-

Any proof that the service wasn’t rendered or the product wasn’t received.

Step 3: Write a Formal Dispute Letter

This is the most crucial step for FCBA protection. While calling the card issuer is a good first step, a written letter is legally required to trigger FCBA protections.

-

What to Include: Your name, account number, the disputed amount, the date of the charge, the merchant’s name, and a clear explanation of why you are disputing the charge.

-

Where to Send It: Send it to the “Billing Inquiries” or “Dispute Resolution” address provided on your credit card statement, not the payment address.

-

Method: Send it via certified mail with a return receipt requested. This provides proof that the issuer received your dispute and when.

Step 4: Stop Payments (Only for the Disputed Amount)

While the dispute is ongoing, you are not required to pay the disputed amount or any finance charges related to it. However, you must continue to pay all other undisputed parts of your bill to avoid late fees and negative credit reporting.

Step 5: Monitor Your Account and Credit Report

-

Account: Keep an eye on your account statement to see if the disputed amount is temporarily credited back to you during the investigation.

-

Credit Report: Ensure the disputed charge is not reported as delinquent or charged off while the dispute is active. If it is, this can be a serious issue, as incorrect reporting can significantly impact your credit score and influence future applications. Learn more about the factors of credit score in our guide How Long Does It Take to Repair Bad Credit.

4. Potential Outcomes of a Dispute

-

Resolved in Your Favor: The charge is removed, and any temporary credit becomes permanent.

-

Resolved in Merchant’s Favor: The charge remains, and you will be responsible for the original amount plus any accrued interest. You have the right to request documentation from the issuer as to why they sided with the merchant.

-

Negotiation: Sometimes the issuer will mediate a partial refund or resolution between you and the merchant.

5. Final Advice: Proactive Protection

-

Review Statements Regularly: Don’t wait 59 days to spot an error. Check your online statement frequently.

-

Keep Records: Always save receipts, especially for large purchases, services, or online orders.

-

Know Your Card: Understand the specific fraud and dispute policies of your card issuer, as some offer protections beyond the FCBA.

-

Understanding Rejections: If you face a denial for a future card because of a poor credit history due to past issues, understanding common denial reasons can help you prepare a stronger application next time. For further reading, consult: Credit Card Application Denial Common Reasons.

Conclusion: Knowing how to dispute a credit card charge is an essential aspect of responsible credit card management in 2026. By understanding your rights under the Fair Credit Billing Act, acting promptly, and meticulously documenting your case, you empower yourself to resolve errors, fight fraud, and protect your financial well-being against unauthorized or incorrect transactions. This consumer protection mechanism ensures that your credit card remains a reliable and secure tool for everyday life.

Credit Score Unlocked: The 2026 Definitive Guide

Credit Cards and Business Success: Your 2026 Essential Guide