Debt Consolidation Loan vs Balance Transfer Credit Card: The 2026 Ultimate Comparison

Debt Consolidation Loan vs Balance Transfer Credit Card: The 2026 Ultimate Comparison

High-interest credit card debt can quickly become an overwhelming burden, trapping US consumers in a cycle of minimum payments that barely touch the principal. For those seeking to regain control and accelerate their path to financial freedom, debt consolidation is a powerful strategy. The two most prominent tools for consolidating credit card debt are the debt consolidation loan and the balance transfer credit card. While both aim to reduce your overall interest burden and simplify repayment, they achieve this through fundamentally different mechanisms, each with distinct advantages, disadvantages, and ideal use cases. Understanding the nuances of debt consolidation loan vs balance transfer credit card in 2026 is critical to choosing the right strategy for your unique financial situation. This comprehensive guide will provide an ultimate comparison, breaking down every aspect to help you make an informed decision.

1. Core Mechanism: Fixed Term vs. Promotional Period

1. Core Mechanism: Fixed Term vs. Promotional Period

The fundamental difference lies in how these tools manage interest and repayment.

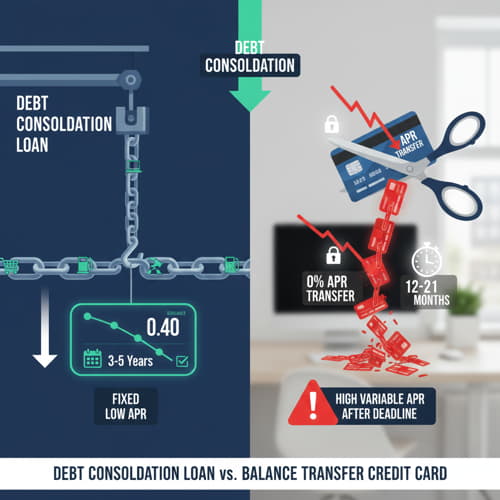

Debt Consolidation Loan (Fixed Term, Predictable Payment)

-

Mechanism: An unsecured personal loan where you borrow a lump sum to pay off all your high-interest credit cards. You then have a single, fixed monthly payment with a set interest rate over a predetermined loan term (e.g., 3-5 years).

-

Interest: A fixed Annual Percentage Rate (APR) that applies for the entire life of the loan. This rate is usually significantly lower than credit card APRs (e.g., 8-15% vs. 20-30%).

-

Fees: Often includes an origination fee (typically 1-8% of the loan amount), which is either deducted from the loan proceeds or added to the principal.

-

Repayment: Structured, fixed monthly payments. You know exactly when your debt will be paid off.

-

Credit Impact: Converts revolving debt (credit cards) into installment debt (loan), which can positively impact your credit mix and utilization.

Balance Transfer Credit Card (0% APR, Race Against Time)

-

Mechanism: A new credit card that offers a 0% introductory APR for a promotional period (typically 12 to 21 months). You transfer your existing high-interest credit card balances to this new card.

-

Interest: 0% APR during the promotional period, meaning 100% of your payments go to the principal. After the intro period, any remaining balance accrues interest at a high, variable APR.

-

Fees: Almost always includes a balance transfer fee (typically 3-5% of the transferred amount), which is added to your new card balance.

-

Repayment: Flexible minimum payments, but you must pay off the entire transferred balance before the 0% APR period expires to avoid significant interest charges.

-

Credit Impact: Can temporarily lower credit utilization, but the debt remains revolving. High balances after the intro period can harm your score.

2. Credit Score & Eligibility: Who Qualifies for What?

Your credit score is a major determinant in which option is available to you.

Debt Consolidation Loan

-

Eligibility: Generally requires a good to excellent credit score (FICO 670+ for the best rates). Some lenders may offer loans to those with fair credit (600-669), but with higher interest rates.

-

Approval: Based on your credit history, debt-to-income ratio, and income stability.

Balance Transfer Credit Card

-

Eligibility: Typically requires excellent credit (FICO 720+) to qualify for the longest 0% intro periods and highest credit limits. Good credit (670-719) might qualify for shorter intro periods.

-

Approval: Heavily reliant on a strong credit score and low credit utilization on existing accounts.

3. The Risks and Rewards: Discipline vs. Predictability

The choice often comes down to your financial discipline and preference for risk.

Debt Consolidation Loan

-

Pros:

-

Predictable: Fixed payments and a clear end date.

-

Lower APR: Typically significantly lower than credit card APRs.

-

Simplicity: One monthly payment instead of many.

-

Removes Temptation: Once credit cards are paid off, you can close them to avoid new debt.

-

-

Cons:

-

Always Pay Interest: Even at a lower rate, you are always paying some interest.

-

Origination Fee: Can add a few hundred dollars to the total cost.

-

Fixed Payments: Less flexibility if you face a financial emergency.

-

Balance Transfer Credit Card

-

Pros:

-

Potential for Zero Interest: If paid off completely, it’s the cheapest option.

-

Flexible Payments: Minimum payments can be low if needed (but should be avoided).

-

-

Cons:

-

The Deadline: The biggest risk. Missing the deadline means high retroactive interest (on some cards) or a high go-to APR on the remaining balance.

-

Balance Transfer Fee: An upfront cost.

-

Temptation to Spend: The open credit line on the new card makes it easy to accumulate new debt.

-

Requires High Discipline: Demands a strict budget and payment plan.

-

4. Strategic Considerations for 2026

Before making your choice, consider these factors:

A. The Size of Your Debt

-

Small to Moderate Debt (Under $10,000): A balance transfer card is often ideal if you can pay it off within 12-18 months.

-

Large Debt (Over $10,000): A personal loan might be safer due to its fixed payments and longer terms, especially if a balance transfer card’s limit isn’t high enough, or you’re unsure you can pay it off in 21 months. For those considering paying off high-interest debt, our guide on the Best Way to Pay Off High Interest Credit Card Debt offers further insights.

B. Your Financial Discipline

-

Highly Disciplined: If you can commit to a strict budget and aggressive payments, a balance transfer offers the best savings.

-

Needs Structure: If you struggle with self-control or deadlines, a personal loan’s fixed payment structure might be more effective.

C. Your Goal for Credit Cards

-

Eliminate and Forget: A personal loan helps you close old cards and start fresh.

-

Manage and Keep: A balance transfer allows you to keep credit lines open, which can benefit your length of credit history and overall credit utilization, if managed perfectly. Regularly monitoring your financial health is crucial, especially if you are concerned about your financial future. Learning How to Use a Credit Card Responsibly for Beginners is the first step in this journey.

In conclusion, the decision between a debt consolidation loan vs balance transfer credit card boils down to your credit profile, the amount of debt, and your personal financial habits. Both are powerful tools for escaping high-interest credit card debt in 2026. The balance transfer offers the potential for zero-interest freedom, demanding high discipline. The personal loan offers predictability and a clear path, sacrificing some potential interest savings for peace of mind. Choose the strategy that aligns best with your ability to commit and control your spending.

Best Way to Pay Off High Interest Credit Card Debt: Strategies for 2026

What Happens If I Only Pay the Minimum on My Credit Card? The Trap of Long-Term Debt