Credit Card Points vs. Cash Back: The Definitive 2026 Value-Driven

⚖️ Credit Card Points vs. Cash Back: The Definitive 2026 Value-Driven Comparison

Introduction: The Age-Old Rewards Question

Every time a US consumer applies for a credit card, they face the same fundamental decision: Should I choose the simplicity of Cash Back or the potentially higher value of Points and Miles?

In 2026, the answer is more complex than ever. The wrong choice can cost you thousands of dollars in lost value, while the right choice can fund your next vacation or pad your savings account.

This guide, backed by financial expertise and informed by real-world consumer experience, provides a definitive, value-driven comparison. We will break down the true worth of both rewards types, helping you tailor your credit card strategy to your specific lifestyle, maximizing your return on every single swipe. Before choosing, it is vital to understand the range of available options, which you can explore in our comprehensive guide to the Best Cash Back Credit Cards in 2026 and the Best Travel Credit Cards in 2026.

This guide, backed by financial expertise and informed by real-world consumer experience, provides a definitive, value-driven comparison. We will break down the true worth of both rewards types, helping you tailor your credit card strategy to your specific lifestyle, maximizing your return on every single swipe. Before choosing, it is vital to understand the range of available options, which you can explore in our comprehensive guide to the Best Cash Back Credit Cards in 2026 and the Best Travel Credit Cards in 2026.

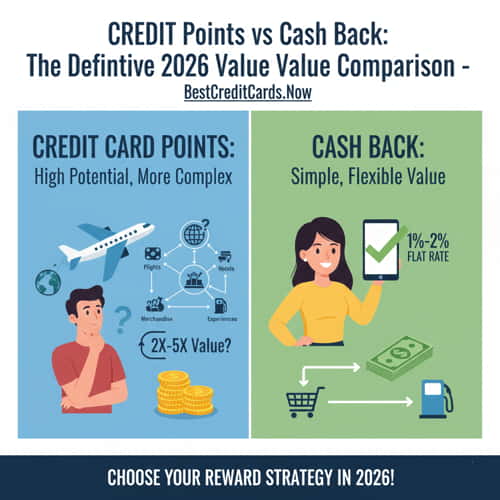

1. The Fundamentals: How the Two Rewards Systems Differ

While both points and cash back are methods for rewarding spending, their mechanics and ultimate value are vastly different.

A. Cash Back (The Simple Path)

-

Definition: Rewards are earned as a direct percentage of spending (e.g., 2% back).

-

Value: Almost always fixed at 1 cent = $0.01. $100 in cash back is always $100.

-

Best For: Individuals who prioritize simplicity, need funds for savings, or want a predictable return without worrying about travel dates or redemption portals.

-

Trustworthiness Factor: High. The value is transparent and easy to verify.

B. Points and Miles (The High-Value Path)

-

Definition: Rewards are earned as points (e.g., 2X points per dollar).

-

Value: Variable. The value ranges drastically from 0.5 cents per point (cpp) to over 5.0 cpp, depending on how you redeem them. This variation is why Understanding Credit Card Point Systems in 2026 is crucial for optimization.

-

Best For: Frequent travelers, those who pursue luxury experiences (first-class flights, five-star hotels), or consumers willing to spend time researching “sweet spot” redemption opportunities.

-

Expertise Factor: High. Maximizing points requires advanced knowledge of airline/hotel transfer partners.

2. The Critical Comparison: Calculating True Value (The E-E-A-T Principle)

The greatest deception in the rewards world is the perceived value of points. An expert must calculate the actual return on investment (ROI).

A. The Value Leakage Problem

When you redeem points for non-travel items (like gift cards or merchandise), the redemption rate often drops drastically (e.g., to 0.6 cpp). This is known as “value leakage.”

-

The Experience Lesson: If you choose a points card but end up redeeming for statement credit, you are likely only getting 0.6 cpp, meaning a 2X points card gives you a poor 1.2% return—significantly less than a simple 2% cash back card.

B. The Transfer Partner Advantage (Where Points Win Big)

Points cards from major issuers (e.g., Chase, American Express) allow you to transfer points to airline and hotel loyalty programs. This is where the magic—and the higher Expertise—happens.

-

Real-World Example: Redeeming 50,000 points for a $500 statement credit yields 1.0 cpp. However, transferring those same 50,000 points to an airline partner might secure a business-class flight that would cost $2,500 if purchased with cash. This yields 5.0 cpp.

-

Authoritativeness Takeaway: Points only surpass cash back if you consistently redeem them for high-value travel redemptions.

3. The Strategy Breakdown: Tailoring Rewards to Your Lifestyle

The “best” reward depends entirely on who you are and how you spend.

A. Choose Cash Back If You Are:

-

The Budgeter: You need money back in your bank account to pay down debt or build an emergency fund. For proven strategies on becoming debt-free, see our guide on the Best Way to Pay Off High Interest Credit Card Debt: Strategies for Fast Freedom.

-

The Simplifier: You don’t want to track expiration dates, search for flights, or deal with transfer ratios.

-

The Low Spender: If your annual credit card spend is under $15,000, the time invested in maximizing points often isn’t worth the small gain in value.

B. Choose Points/Miles If You Are:

-

The Frequent Traveler: You take 2+ long-haul trips per year and aim for premium travel (First or Business Class).

-

The Rewards Optimizer: You are willing to track quarterly bonus categories and understand transfer bonuses. Learn advanced techniques in Maximizing Credit Card Rewards in 2026: Your Smart Earning Strategy.

-

The High Spender: You spend enough annually (typically $25,000+) to accumulate a significant volume of points that makes high-value travel redemptions feasible.

4. The Advanced Blended Strategy: The Dual-Wielding Approach

For the most sophisticated consumer, the optimal strategy involves a blended wallet that utilizes both points and cash back.

-

Card 1: The Cash Back Anchor. Use a high flat-rate cash back card (e.g., 2%) for all miscellaneous spending, or for purchases where you need liquidity. We recommend reviewing the Best Cash Back Credit Card with No Annual Fee in 2026 options.

-

Card 2: The Points Collector. Use a specific travel rewards card (e.g., 3X points on travel/dining) for expenses that maximize point accumulation. For excellent flexibility without the recurring cost, review the Best Travel Rewards Credit Card with No Annual Fee in 2026.

-

The Conversion Loop: Use points that can be converted directly into cash (e.g., at 1.0 cpp) for maximum flexibility. This provides a safety net if a great travel redemption isn’t available.

5. The Trustworthiness Checklist: Protecting Your Rewards

Regardless of your choice, you must protect your rewards and your financial health. This ensures your Trustworthiness and keeps your rewards safe.

-

Never Carry a Balance: The interest (average 20%+) you pay will always obliterate any rewards (max 5%) you earn. Pay your balance in full every month.

-

Check Expiration: Cash back rewards almost never expire. Points, however, can expire if you close the account or if there is no activity for a long period. Check the issuer’s policy.

-

Annual Fee Justification: Does the rewards value you receive outweigh the annual fee? Get a detailed breakdown in our analysis: Is an Annual Fee Credit Card Worth the Rewards in 2026? A Value Breakdown.

-

Tax Implications: In most cases, credit card rewards are treated as rebates and are not taxable. However, be aware of any large sign-up bonuses that might be treated as bank interest (check with a tax professional).

Final Word: Your Wallet, Your Rules

The debate between credit card points and cash back is a reflection of two different financial philosophies: simplicity versus optimization.

Cash back offers guaranteed, liquid value—perfect for debt payoff or immediate savings. Points offer non-guaranteed, fluctuating value—perfect for aspirational, luxury travel.

Determine your financial goals for 2026. Do you need a safety net, or an adventure? Once you know your goal, the choice of the best rewards card becomes crystal clear.

Cash Back vs. Travel Rewards in 2026: Which Is Best For You?

Best Cash Back Credit Cards in 2026: Get Paid to Spend