Best Balance Transfer Credit Card for Bad Credit in 2026

Best Balance Transfer Credit Card for Bad Credit in 2026: A High-Risk, High-Reward Strategy

For US consumers in 2026 struggling with crippling credit card debt, a balance transfer (BT) is often presented as the ultimate lifeline—a way to shift high-interest debt onto a new card with a 0% introductory APR. However, when your credit profile falls into the “bad credit” category (typically FICO scores below 600), the pursuit of the best balance transfer credit card for bad credit becomes a high-stakes challenge. Most premium 0% BT offers are reserved for applicants with excellent or good credit (690+). The truth is, finding a true 0% APR BT card for bad credit is extremely difficult, but not entirely impossible. This comprehensive guide will dissect the harsh realities of the subprime balance transfer market, outline the limited yet viable alternatives, and—most importantly—provide the strategic roadmap you need to repair your credit first, making a successful, interest-saving balance transfer a future reality.

1. The Harsh Reality of Bad Credit and 0% APR

1. The Harsh Reality of Bad Credit and 0% APR

A balance transfer is a form of risk management for the bank. They are essentially lending you money (interest-free) to pay off another lender. For someone with a history of missed payments or high debt (the definition of bad credit), this risk is astronomical.

A. The Denial Filter

Card issuers offering 0% APR BTs are typically looking for borrowers who are financially stable enough to pay off the debt after the promotional period ends, but not so stable that they wouldn’t need the interest-free period in the first place. Bad credit automatically places you outside this sweet spot.

B. The True Cost of Subprime Cards

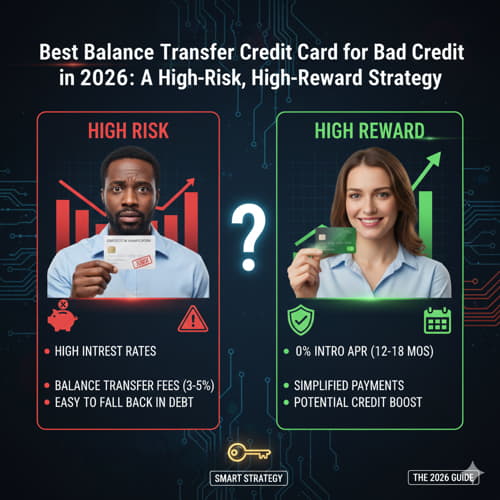

Some cards marketed to consumers with poor credit do allow balance transfers, but they often come with immediate and severe drawbacks:

-

Massive Balance Transfer Fees: Instead of the standard 3% to 5% fee, subprime cards might charge a BT fee of 7% or more.

-

Non-0% APR: The promotional rate might only be a few points lower than your current card (e.g., 18% instead of 25%), which is not a meaningful savings.

-

Short, Unrealistic Terms: The promotional period might only be 6 or 9 months, not enough time to make a dent in large debt.

2. Viable Alternatives to 0% BT Cards for Bad Credit

Since the ideal 0% BT card is unlikely, focus on these achievable alternatives, which are better first steps out of the debt cycle.

Alternative 1: Credit Union Secured Loans or Debt Consolidation

Credit unions are often more lenient and willing to work with members than large national banks.

-

Secured Personal Loan: You might secure a small loan (collateralizing a savings account or CD) at a lower interest rate (e.g., 8-12%) than your credit card (29.99%). This is a fixed, predictable path to debt reduction.

-

Credit Union Secured Credit Card: If you can’t qualify for a loan, a secured card is the definitive first step to rebuilding. You need to start improving your payment history and utilization ratio, which are the fundamental components required for any favorable BT offer in the future.

-

Internal Link 1: This is the essential first step—getting a functional credit card. Focus on: Best Credit Card for Bad Credit with Instant Approval.

Alternative 2: The Self-Managed “Snowball” or “Avalanche” Method

Instead of relying on a new card, focus on aggressively paying down your existing high-interest debt.

-

Snowball: Pay minimums on all cards except the smallest-balance card, which you attack aggressively.

-

Avalanche: Pay minimums on all cards except the highest-interest-rate card, which you attack aggressively.

3. The Strategic Pre-Requisite: Credit Repair

No matter how urgent your debt is, the most valuable strategy is improving your credit score first. A score in the “Fair” range (600-660) opens up vastly better debt options than a “Bad” score.

-

Focus on Payment History (35% of FICO): The immediate priority is ensuring every payment on every debt is on time.

-

Reduce Current Utilization (30% of FICO): Pay down your balances to reduce your utilization ratio below 30%, and ideally below 10%. Even a 50-point score increase can change your eligibility from denial to approval for a lower-interest product.

-

Patience and Consistency: Credit repair takes time. Understanding the timeline and the process is essential to avoid quick-fix traps.

-

Internal Link 2: Learn more about the timeline for credit improvement: How Long Does It Take to Repair Bad Credit.

4. The Balance Transfer Checklist (If You Find an Offer)

If you manage to secure a balance transfer offer, assess it with extreme caution:

Best Way to Pay Off High Interest Credit Card Debt: Strategies for Fast Freedom

Credit Card Debt Consolidation Options Explained Simply in 2026: Your Path to Financial Freedom