Credit Card Balance Transfer vs Personal Loan: The 2026 Guide to Debt Consolidation

Credit Card Balance Transfer vs Personal Loan: The 2026 Guide to Debt Consolidation

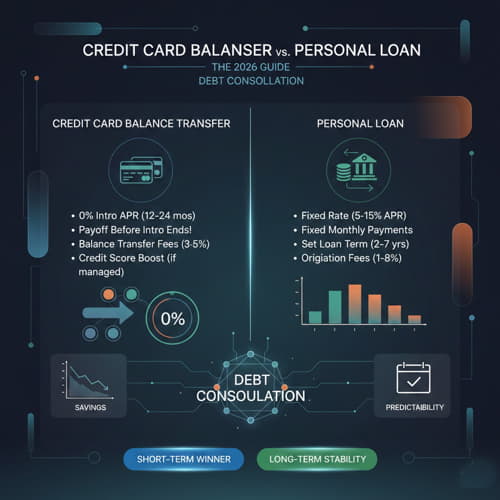

For individuals struggling with high-interest credit card debt in the US, the need for debt consolidation is paramount. Consolidating multiple high-APR debts into a single, lower-cost payment can save thousands of dollars and drastically simplify the path to financial freedom. The two most popular and effective strategies for this are the credit card balance transfer and the personal loan. While both serve the same goal—reducing the interest burden—they operate on fundamentally different mechanics, risk profiles, and timelines. The choice between a credit card balance transfer vs personal loan in 2026 is a critical one that depends entirely on your discipline, credit score, and how quickly you can achieve debt freedom. This comprehensive guide breaks down the pros, cons, and mechanics of each option to help you select the most optimal path for your specific financial situation.

Mechanism Breakdown: 0% APR vs. Fixed Installment

Mechanism Breakdown: 0% APR vs. Fixed Installment

The core difference between the two methods lies in their interest structure and repayment schedule.

Best Balance Transfer Credit Card for Bad Credit in 2026

Credit Cards and Budgeting: Your 2026 Guide to Spending